The water crisis is no longer the elephant in the room; government leaders, scientists and innovators have brought the plight of SDG 6, clean water and sanitation, to centre of sustainable development discussions. Between 2015-2020, 107 million people have gained access to safe drinking water and 115 million people have gained safe access to toilets at home (CDC 2022). However, data from the World Health Organisation (WHO) indicate that over 2 billion people still lack access to clean drinking water. The evidence for the water crisis is undeniable.

The World Economic Forum has identified the water crisis as one of the top 5 global risks to impact society. If ‘step 1’ in solving the crisis is identifying and acknowledging that failings for SDG 6 poses a global threat, what is ‘step 2’ and how do we get there?

Let’s break down some of the most prevalent barriers standing in our way from reaching SDG 6:

1. FUNDING GAP

Various estimates exist that have attempted to quantify the total funding required to achieve SDG 6, however a precise answer appears vague and somewhat elusive.

In 2016, one year after the sustainable development goals were established, the estimated funding required to meet all of the targets for SDG 6 was valued at 114 billion USD. This figure was problematic; it did not account for replacing old infrastructure, the maintenance and management of WASH infrastructure, nor did it include the cost of making the WASH sector climate resilient.

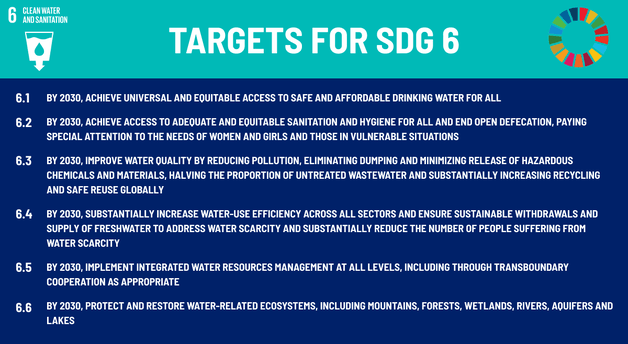

In the breakdown of SDG 6 targets (see figure 1), the World Bank has now estimated that 114 billion USD / annum will be needed to achieve targets 6.1 and 6.2 alone.

Other estimates for the total funding for SDG 6 vary: Global Waters pins the total required funding as 263 billion. However, funding for the WASH sector has been reported as relatively stagnant since 2016. Scaling innovating modes of financing will be key to overcoming this challenge in 2023 and beyond.

Figure 1 – The Individual Targets for SDG 6 – Clean Water and Sanitation. Adapted from the UN

2. CLIMATE RESILLIANCE

The phrase “climate resilience” has gained more recognition in recent years in the context of funding sustainable development. It is no longer enough for investments to be ‘green’ to have a long-term impact. They must be able to withstand and adapt to present and oncoming climate shocks.

Global warming and rising temperatures have increased the occurrence of natural disasters and climate shocks. Therefore, current and future infrastructures need to be reimagined and re-designed with the foresight of the effects of global warming. Clearly, there is a trade-off – ensuring that WASH investments are climate resilient will have attributed costs. However, if these investments are ill-structured to cope with the impacts of global warming, the damage – social, environmental and economic – will be far greater.

“The incremental cost of ensuring new water and sanitation assets are climate-resilient is estimated to be between $0.9 billion and $2.3 billion a year, which represents around 1 per cent of baseline infrastructure investment needs and would reduce the risk of damage to new infrastructure by 50 per cent.”

- ISSD

3. INFLATION

Funding for the SDGs saw a drop during the COVID-19 pandemic (OECD 2020). The world came to a halt, and with it briefly, sustainable development. A report published by OECD estimated that developing countries saw a drop of USD 700 billion from private finance channels. Global supply chains were disrupted, leading to a rise in commodity costs, spurring inflation across global networks (J.P. Morgan Chase 2021).

As pension funds and (investment) banks have historically avoided investments in micro-finance projects surrounding commodity supply chains, the economic burden to try to reduce the impact of inflation from disrupted supply chains fell primarily on governments (van den Breul et al. 2018).

Global conflicts, such as the Russia-Ukraine war have played a role in accelerating inflation through additional supply chain disruption (Aurora and Sarker 2023), the impact of which was felt internationally; many African countries saw disrupted financial markets and increased risk aversion from investors. Government funding was also funnelled towards essential services and goods, such as vaccine research and production, PPE and supporting millions of people with the unemployment and the cost of living crisis with reduced income.

These efforts were wholly and ethically necessary, however the global crisis of COVID-19 and the Russia-Ukraine conflict took precedence over sustainable development funding, increasing the financial gap for government-sourced funding and increasing the reliance on private market funding.

4. FUNDING THE 'MISSING MIDDLE'

The so-called ‘missing middle’ is the funding gap in parts of the finance landscape not met through charitable foundations, microfinance institutions, commercial banks and/or formal capital markets. Small and medium enterprises (SMEs) are often victims of the ‘missing middle’ despite being drivers of sustainable development. SMEs represent a sector with the largest industrial operations but collectively have limited access to resources (WWF 2017).

SMEs that work within the WASH sector play a pivotal in achieving SDG 6. “Blue” SMEs are reported to have restricted growth due to a lack of funding (Garrido 2022). However the tide is changing. For example, the AGF (African Guarantee Fund) partnered with the National Bank of Kenya to aid funding through providing collateral for WASH sector SMEs to overcome the financing barrier (Mutimawase 2022), an example of a successful partnership in aid of SDG 6.

In under two years Water Unite Impact has developed a sizeable investment pipeline, demonstrating that the ‘missing middle' thesis is viable. Over 150 companies have been screened, with in-depth due diligence conducted on 15 different entities in the water sector across Africa, Asia and Latin America and 4 investments made. These investments have provided catalytic capital, driving innovation and helping communities tackle specific challenges at scale in a sustainable, long-term fashion.

5. SELECTIVE FUNDING WITHIN SDG 6 - THE "SEXIER" TARGETS

Although 9% of global NDCs relate to SDG 6, only 2% were linked with access to sanitation and 3% to wastewater treatment (de Albuquerque 2021). Considering that universal access to safe drinking water, adequate sanitation and hygiene has the potential to reduce the global disease burden on healthcare systems by 10% (CDC 2022), it appears that sanitation-specific funding and development is often shunted to the side to favour more “attractive” investments in the WASH sector and beyond.

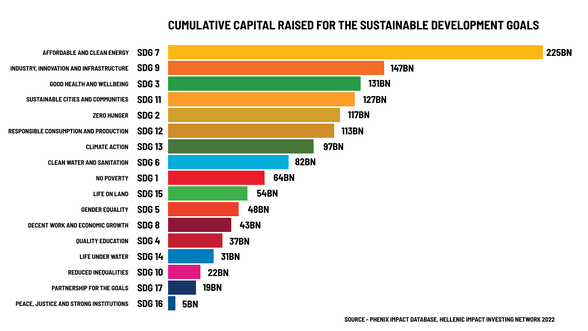

Figure 2 – Cumulative Capital Raised for the Sustainable Development Goals, source – Phenix Impact Database, Hellenic Impact Investing Network

One of the primary funding issues is that for many WASH-related investments, the upfront (Capex) cost is covered but the operational (Opex) cost is not. Using a water pump example, the cost of the concrete, the pump and its parts may often be covered by a charity or NGO. However, the operational cost, including maintenance, repair, electricity and utility costs are, in some instances, unplanned or not covered by the original NGO. Other investments and projects that are more in-line with circular economy theory can circumvent this issue by generating an end product that enables the project to cover the future Opex cost and sustain itself financially e.g. a sustainable business model. Many traditional water pumps, bore holes and other immediate need solutions cannot do this and funding will have to be generated externally over the long term.

So, can we achieve SDG 6? Perhaps this is the wrong question to ask. We can unite and form a global front for sustainable development and in many instances we have, for example through partnerships, coalitions and events such as COP. However, awareness isn’t the problem. The problem is action and funnelling capital towards productive, sustainable action that would enable us to achieve all aspects of SDG 6, with less focus on bureaucracy and ‘back patting’ and more action for the immediate threat of climate change. We’re looking forward to rolling our sleeves up and getting to work in 2023.